Boris Johnson says October 15 is the Brexit deadline

Take control of your international payments with CXI FX Now.

• Low transfer fees & great rates

• Fast international payments

• Safety and security

• Unparalleled customer service

• Consultative approach

Get real-time market coverage on twitter at @EBCTradeDesk or sign up to currency insider here.

SUMMARY

- British PM says both sides should “move on” if no trade deal agreed by then.

- UK’s Internal Market Bill set to undermine parts of Withdrawal Agreement.

- Sterling traders forced reprice-in “no-deal” risks they priced out this summer.

- GBPUSD off 200pts from Friday’s NY close, leading USD broadly higher.

- October WTI plunges 7% after Saudi Aramco’s lowers prices to Asian buyers.

- Nasdaq revisits Thursday lows, still looking for blood after Softbank news.

ANALYSIS

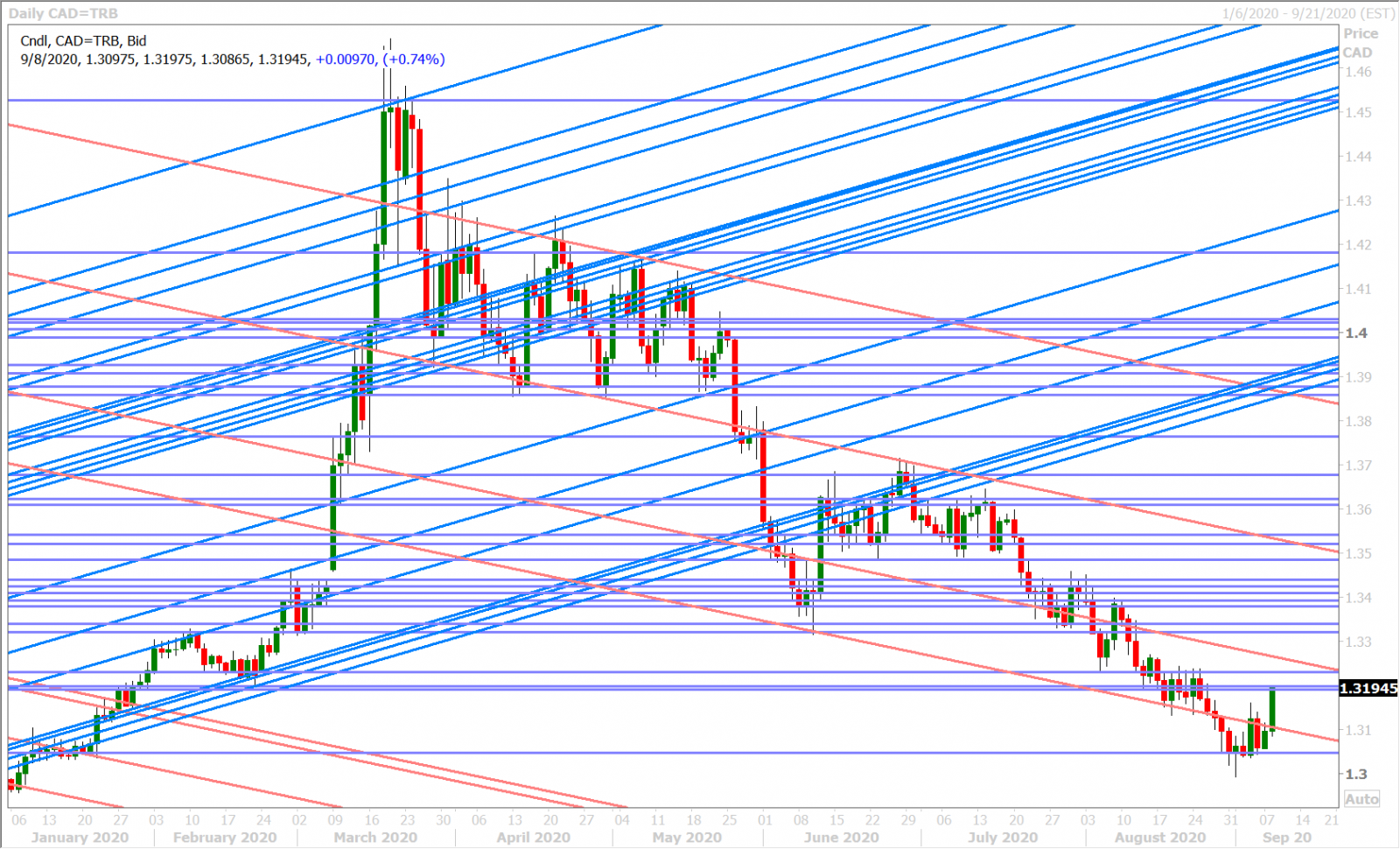

USDCAD

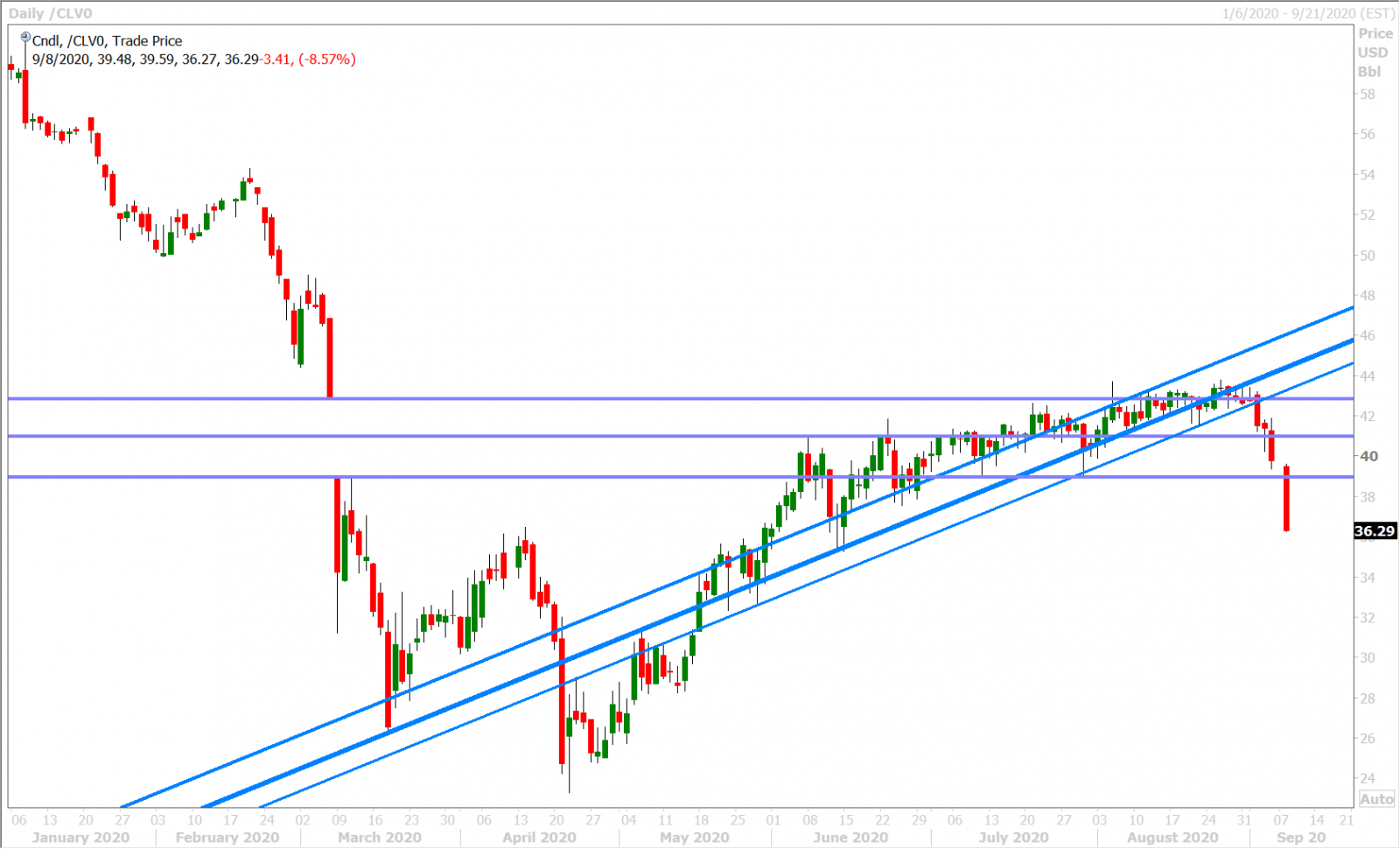

“No deal” Brexit risks are on the rise to start the week after British Prime Minister Boris Johnson said the UK and EU should “move on” if no trade deal is agreed by October 15 and after the Financial Times reported that Johnson’s government is planning legislation to override parts of the Withdrawal Agreement it signed in January. While some analysts say the latter is media-overreaction to the UK’s Internal Market Bill to be released on Wednesday (which seeks to tie up well-known loose ends/ambiguities in the event of a worse-case scenario), sterling traders have decided to reprice-in the possibility of a “no-deal” outcome after months of completely pricing it out. This has sparked a 200pt drop for GBPUSD, a broad USD bid, and a risk-off tone to the broader markets which has now helped USDCAD break strongly back above the 1.3110s resistance level it lost on Friday. October WTI’s 7.5% plunge is adding some fuel to the fire and this seems to be a delayed reaction to the long weekend news of Saudi’s Aramco lowering its official selling prices (OSPs) to Asia amid signs of tepid demand.

Today’s North American calendar is a rather quiet one, which should leave traders focused on Brexit headlines and the fallout from Tesla not making the S&P500 late on Friday. The Nasdaq also looks like it may want to further punish the “Softbank whale” trades that were unmasked by ZeroHedge late last week as one of the big drivers behind this summer’s tech rally. This week’s key feature will be the Bank of Canada decision on Wednesday, but market participants aren’t expecting any major changes to the monetary policy statement, especially given the fact that there won’t be an MPR and a press conference afterwards…although Governor Tiff Macklem could provide soundbites on Thursday morning during his speech at the Canadian Chamber of Commerce.

This week’s calendar also features some US inflation data (August PPI on Thursday/August CPI on Friday) and a large 1.1BLN USDCAD option expiry at the 1.3225 strike on Friday. There won’t be any Fed-speak as the FOMC now enters its black-out period ahead of next week’s policy meeting. The leveraged funds at CME reduced their net long USDCAD position for the second week in a row during the week ending September 1, but we think this morning’s strong move through the 1.3110s now puts the short-term momentum on their side for a change.

USDCAD DAILY

USDCAD HOURLY

OCT CRUDE OIL DAILY

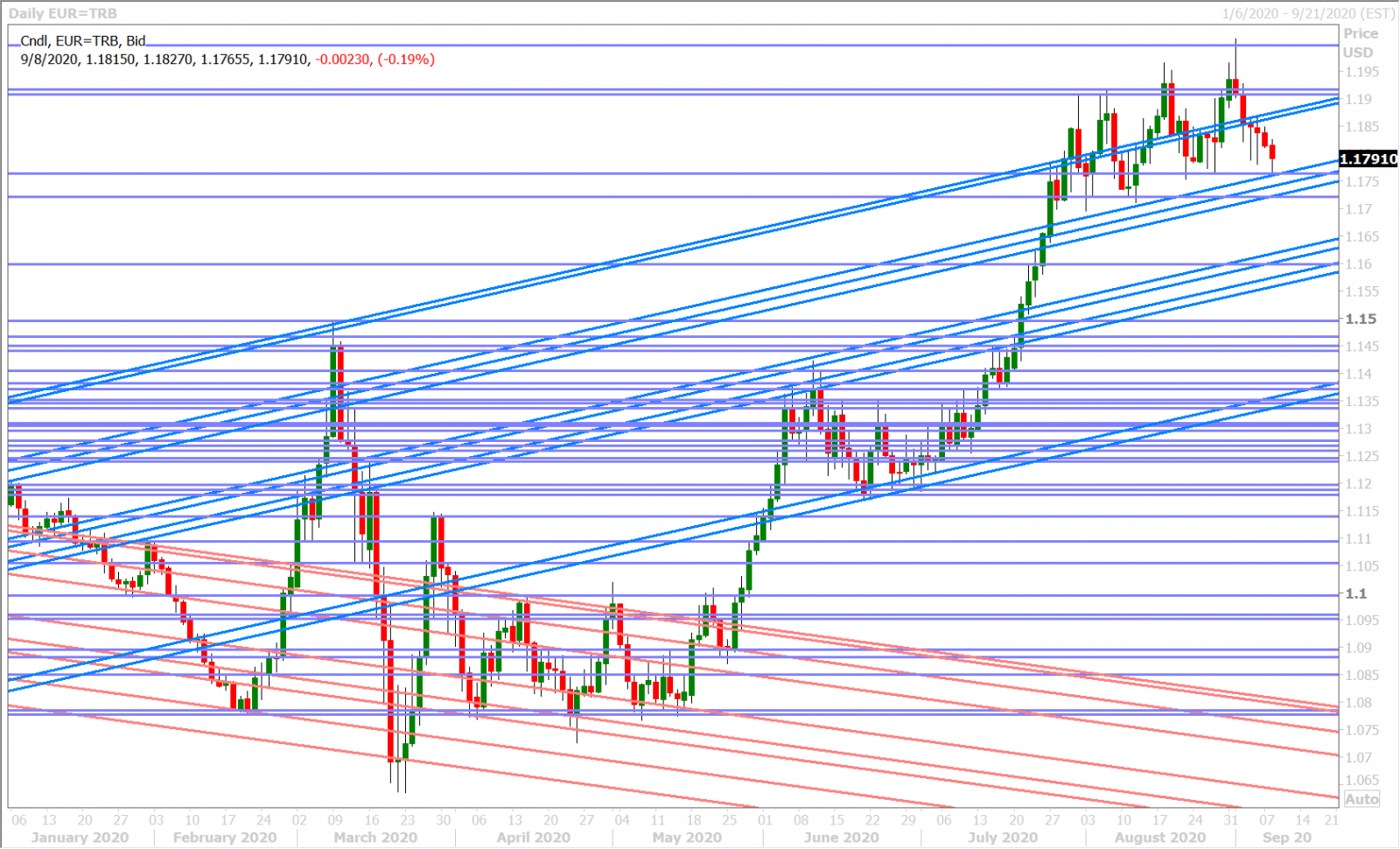

EURUSD

Euro/dollar is pulling back this morning amidst broad USD buying, but we’d note a continuation of the relative outperformance we first saw re-emerge during last Thursday’s stock market rout…and so we ask the question…does the marketplace want to start treating the Euro as a relative safe-haven again (like it did in February)…at least against risk currencies? Two days does not make a trend, but we’re going to keep watching this.

Weaker than expected German Industrial Output data didn’t have much effect on the market yesterday, nor did today’s soft German export data. This week’s key European feature will be the ECB meeting on Thursday, and market participants are now expecting Christine Lagarde to address the euro/dollar exchange rate in light of Philip Lane’s comments last week and the Financial Times article which said its ECB sources are now “worried” about it.

The leveraged funds trimmed back their record long EURUSD position by liquidating longs and adding to shorts during the week ending September 1, and it seems as though the market’s bearish reversal off 1.2000 was the trigger. Thursday’s large, post-ECB meeting, option expiries center around the 1.1775 to 1.1800 strikes (2.8BLN in total), which suggest EURUSD doesn’t do much until then.

EURUSD DAILY

EURUSD HOURLY

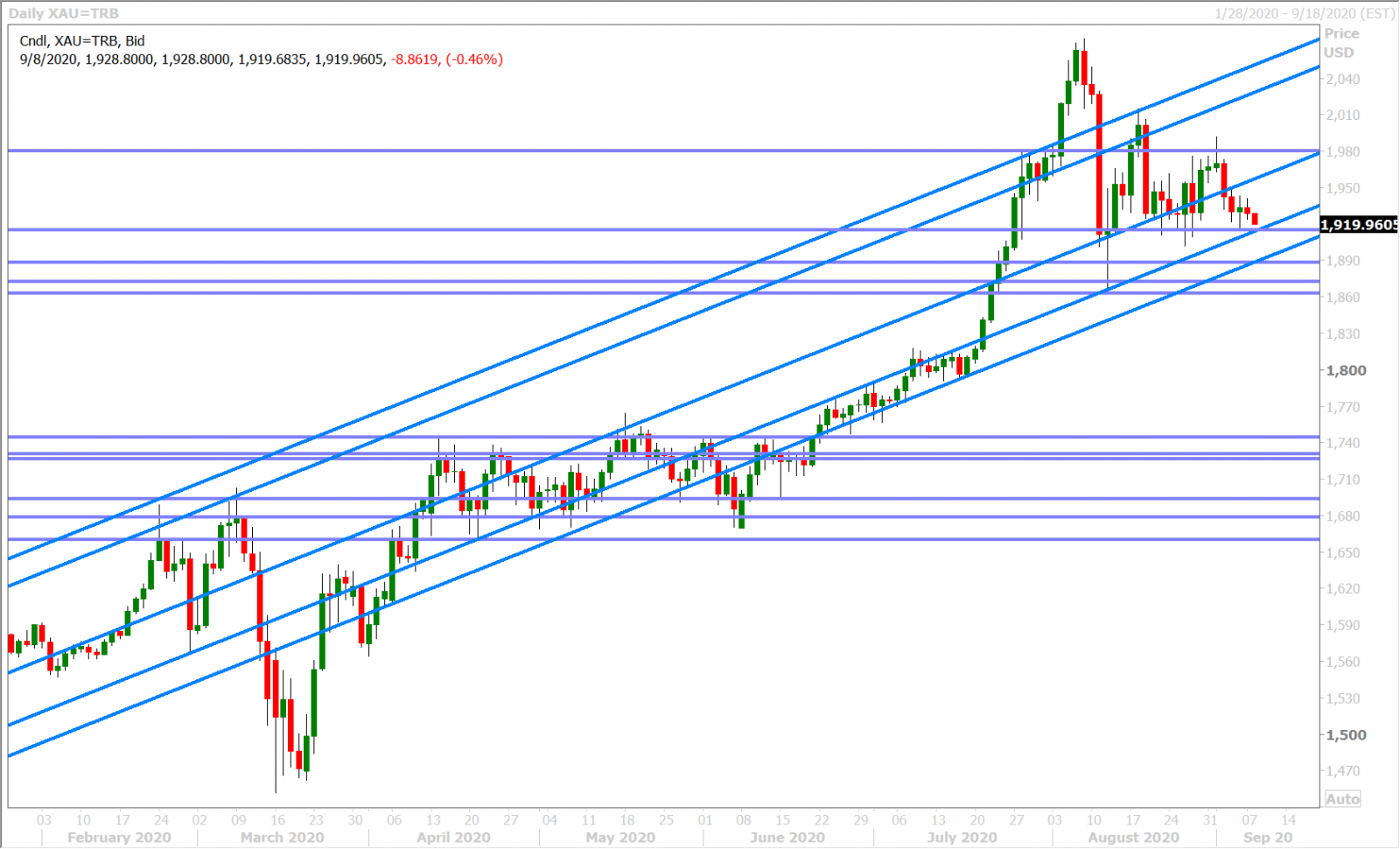

SPOT GOLD DAILY

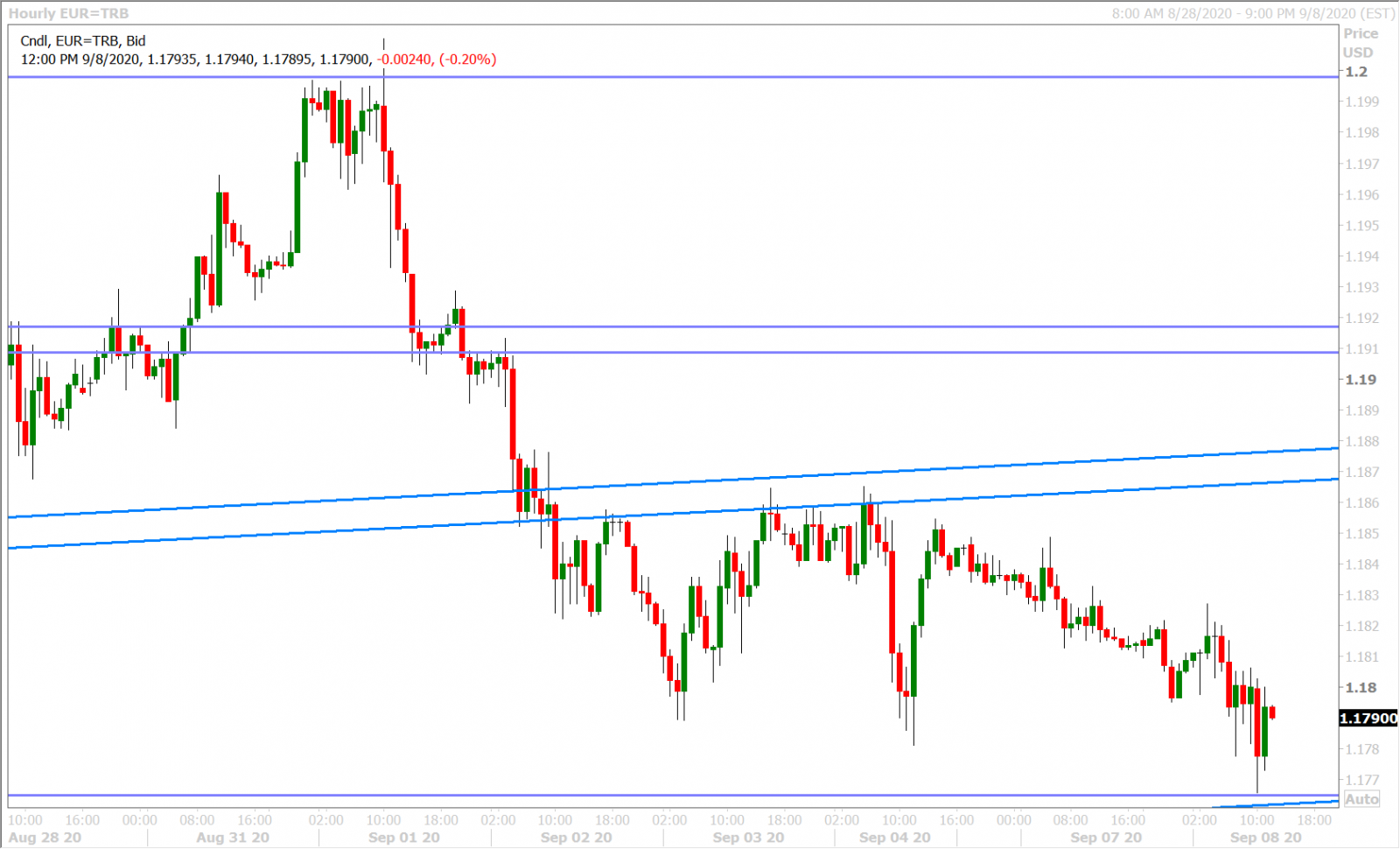

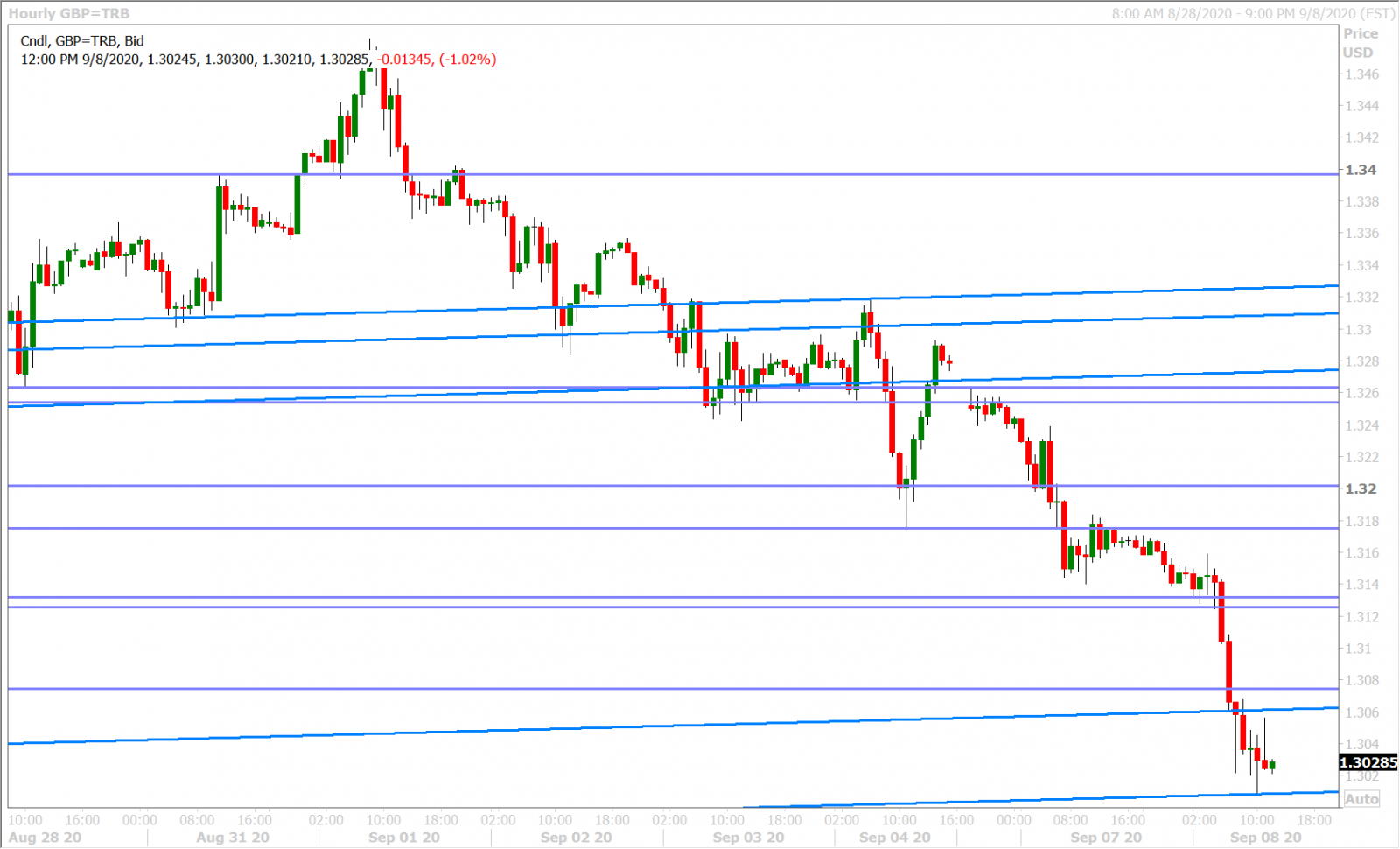

GBPUSD

It’s quite amazing how this weekend’s UK news cycle has dramatically put the market’s focus back on repricing-in “no-deal” Brexit risks it priced out over the summer. The speculative fund community learned the hard way over the last few months that it didn’t pay to hang on to overcrowded, Brexit-themed, bearish bets against the pound amidst broad USD weakness, but they’re now getting their hands handed to them again by holding on to a net long GBPUSD position into Boris Johnson’s threat of “moving on” come October 15. One could make the argument that Boris Johnson’s new deadline is a negotiating ploy and that the merits behind the Internal Market Bill are justified and well known, but we don’t think there’s any denying that the marketplace became a little too complacent on the thought of EU/UK negotiators figuring everything out again at the 11th hour.

We think sterling/dollar’s 200pt decline since Friday’s NY close is a fair reflection of the market’s desire to re-price for some Brexit “no-deal” risk, and we’d note Sunday night’s break below the 1.3220-1.3250 price range as a contributory factor towards GBP selling. Over 800M in options will be expiring at the 0.8950 strike in EURGBP on Thursday (80pts below current pricing), which has us wondering if this week’s Brexit negotiations will see some cooler heads prevail.

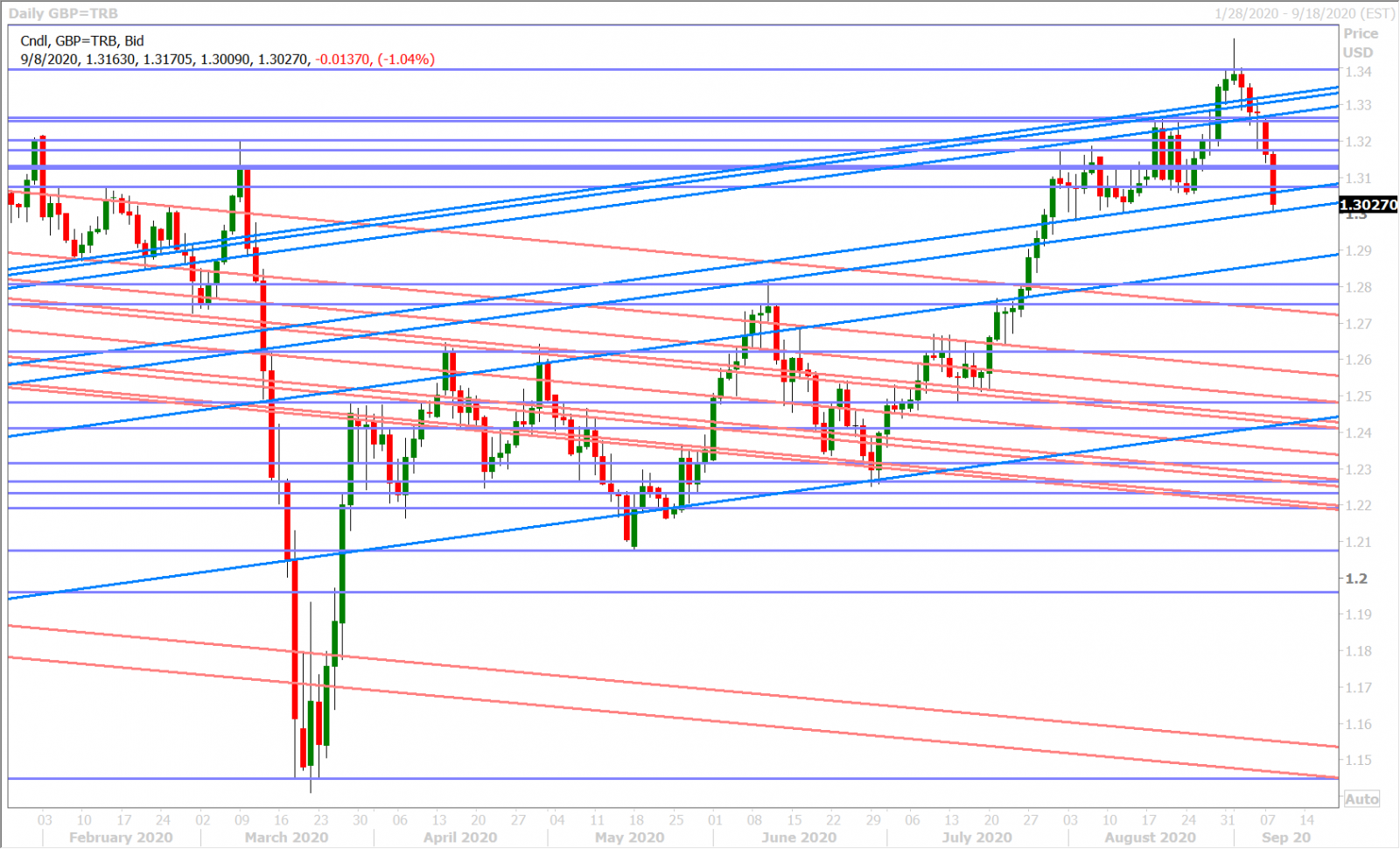

GBPUSD DAILY

GBPUSD HOURLY

EURGBP DAILY

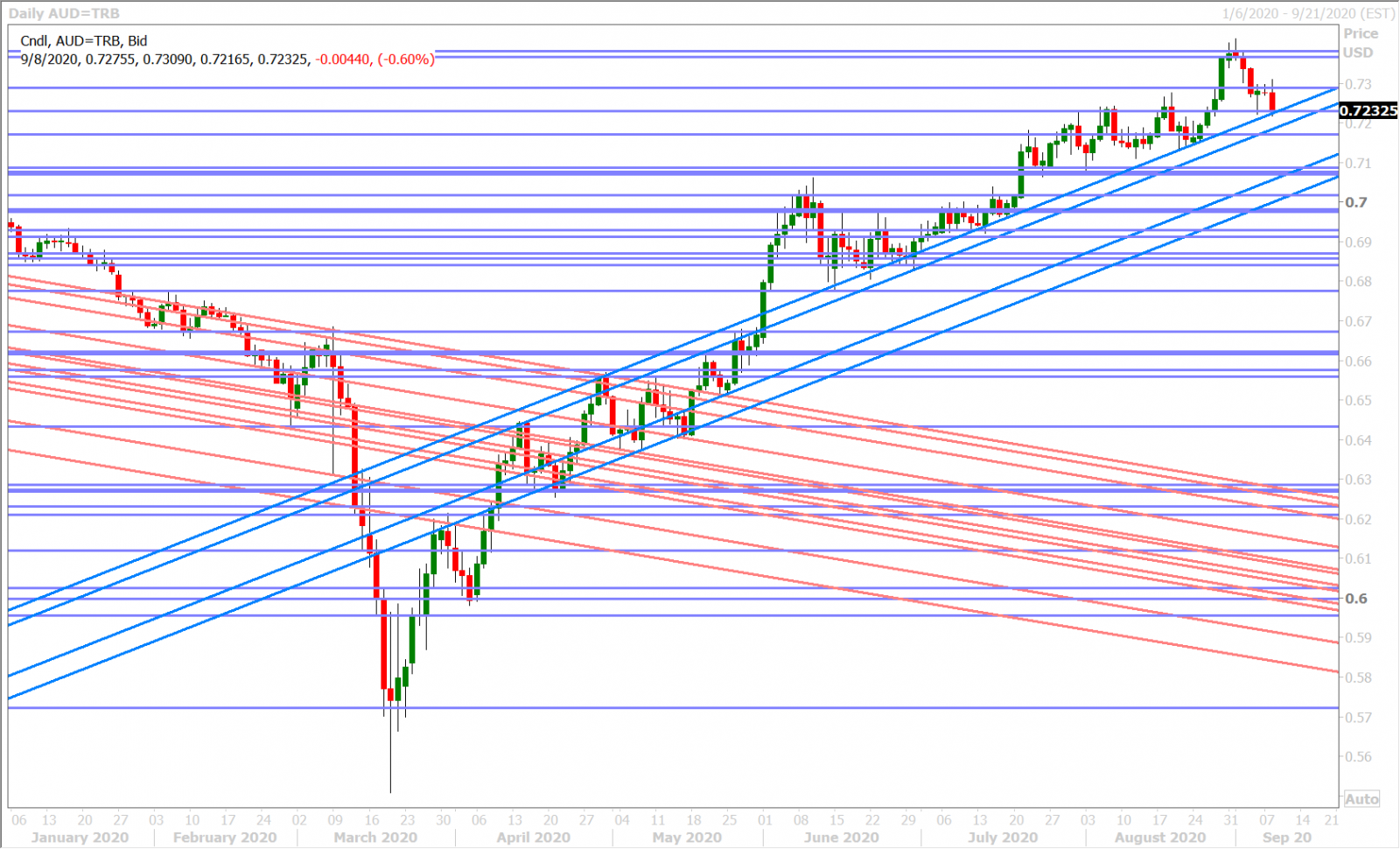

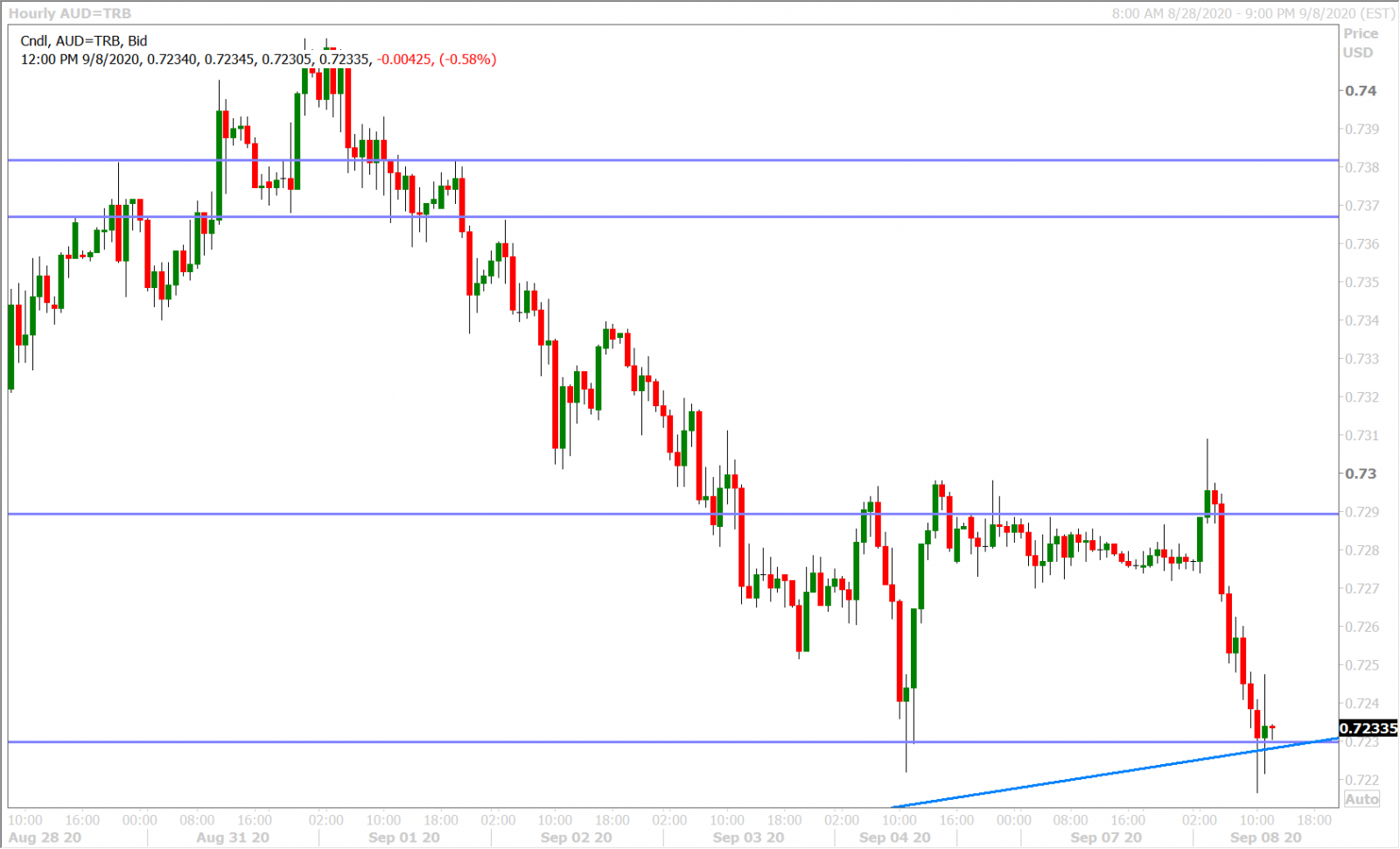

AUDUSD

The Australian dollar defended chart support in the 0.7230s on Friday after the Nasdaq rebounded into the NY close, but it’s putting pressure on this support level once again this morning as the tech index opens 2% lower. This week’s quiet Australian calendar should leave traders focused on broader risk sentiment and the multitude of AUDUSD option expiries between 0.7175 and 0.7300. The leveraged funds at CME trimmed their small net short AUDUSD position to flat during the week ending September 1.

AUDUSD DAILY

AUDUSD HOURLY

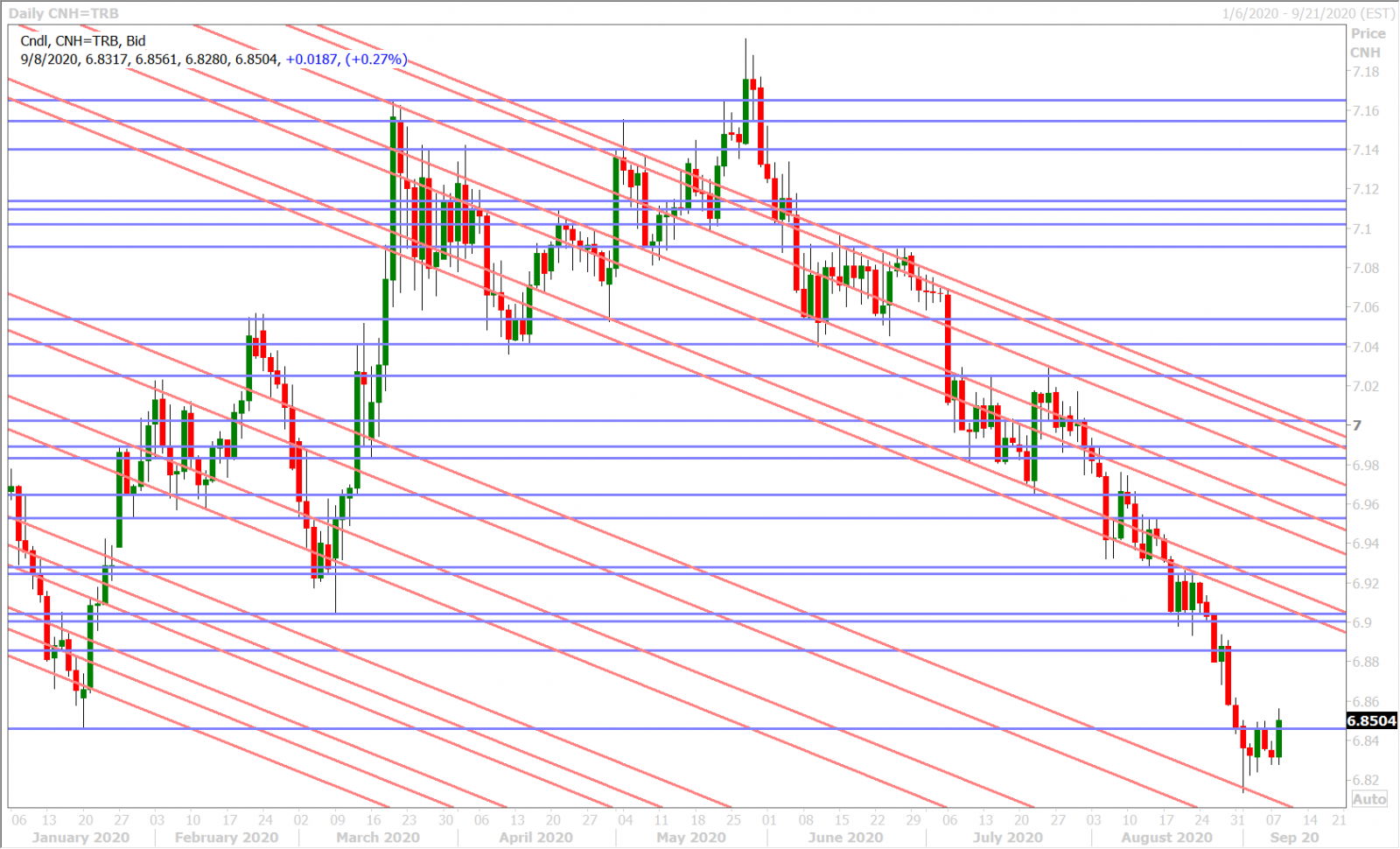

USDCNH DAILY

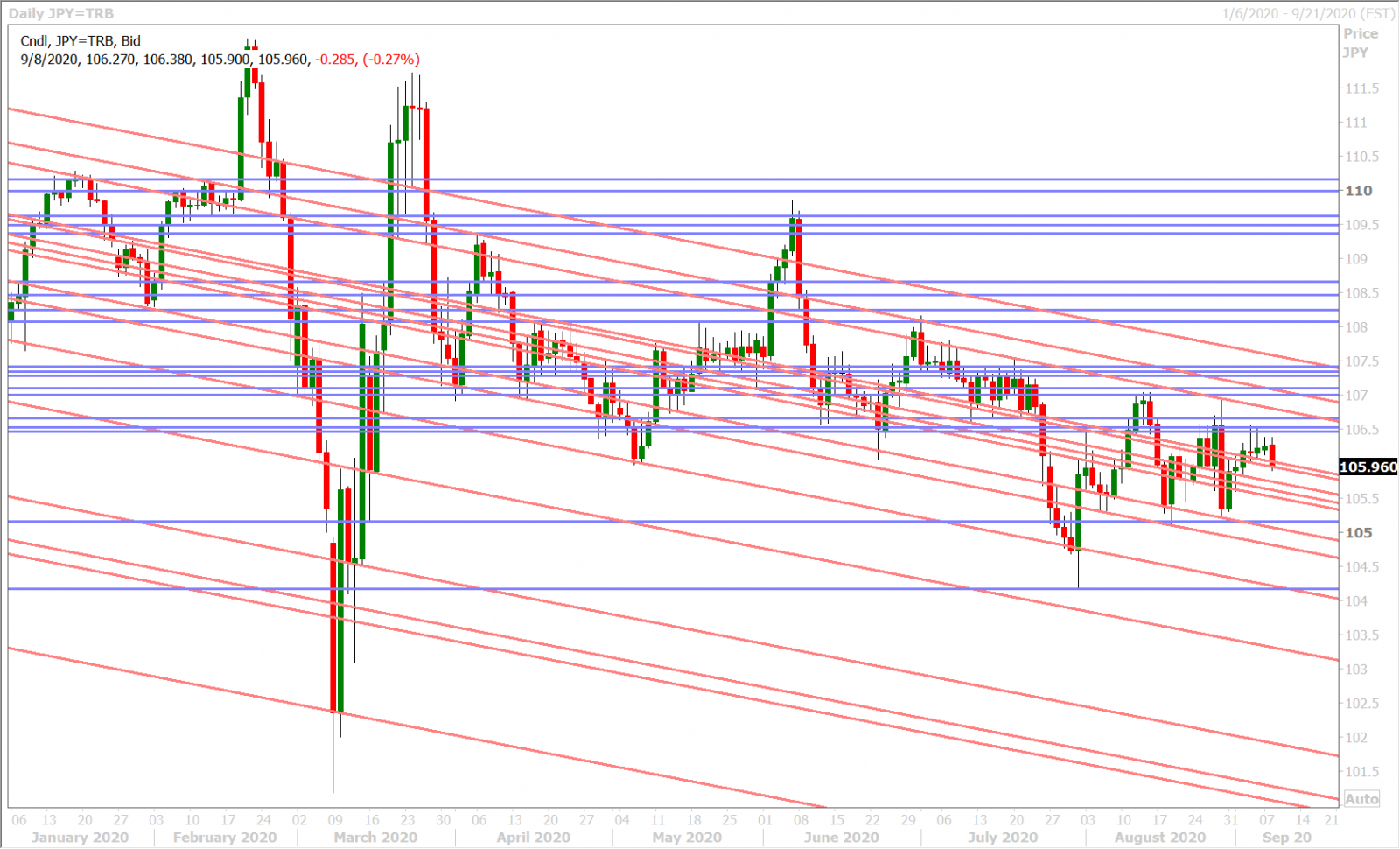

USDJPY

Dollar/yen had an extremely quiet start to the week yesterday as US bond markets were closed for the Labour Day holiday, and while we’ve now seen the market put some pressure on familiar chart support at the 105.90-106.00 area, we’re not really seeing a directional tone to prices.

Chief cabinet secretary Yoshihide Suga has reiterated himself as Japan’s continuity candidate for the LDP leadership race next week but we think markets have now priced in his expected victory. A ton of USDJPY option expiries feature between the 105.50 and 106.50 strikes for Wednesday/Thursday, which could further contribute to the rather dull price action we’re seeing so far this week. Japan reports its July Machinery Orders data at 7:50pmET tomorrow night (+1.9% MoM expected).

USDJPY DAILY

USDJPY HOURLY

US 10YR BOND YIELD DAILY

Charts: Reuters Eikon

About the Author

Erik Bregar - Director, Head of FX Strategy

Erik works with corporations and institutions to help them better navigate the currency markets. His desk provides fast, transparent, and low cost trade execution; up to the minute fundamental and technical market analysis; custom strategy development; and post-trade services -- all in an effort to add value to your firm’s bottom line. Erik has been trading currencies professionally and independently for more than 12 years. Prior to leading the trading desk at EBC, Erik was in charge of managing the foreign exchange risk for one of Canada’s largest independent broker-dealers.

Interested in creating a custom foreign exchange trading plan? Contact us or call CXI's trading desk directly at 1-833-572-8933.

Currency Exchange International (CXI) is a leading provider of foreign currency exchange services in North America for financial institutions, corporations, and travelers. Products and services for international travelers include access to buy and sell more than 80 foreign currencies, gold bullion coins and bars. For financial institutions, our services include the exchange of foreign currencies, international wire transfers, purchase and sale of foreign bank drafts, international traveler’s cheques, and foreign cheque clearing through the use of CXI’s innovative CEIFX web-based FX software www.ceifx.com