The Fed disappoints the uber doves but US/China trade war escalation sees global interest rates resume downtrend

Take control of your international payments with CXI FX Now.

• Zero transfer fees & great rates

• Fast international payments

• Safety and security

• Unparalleled customer service

• Consultative approach

Learn more about CXI's international payment services for businesses or call our trading desk directly at 1-833-572-8933.

Get real-time market coverage on twitter at @EBCTradeDesk or sign up here.

SUMMARY

ANALYSIS

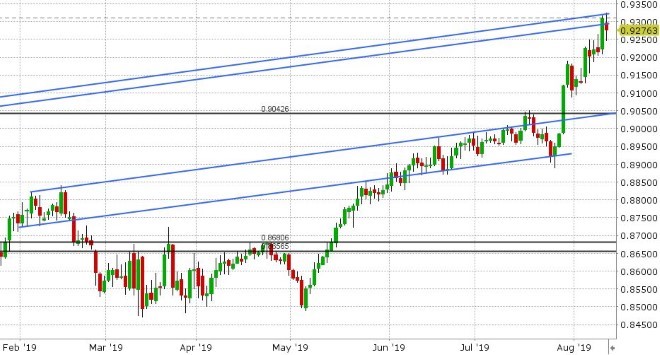

USDCAD

It’s been a volatile past two weeks for much of the G7 FX space and it all got started with the Fed’s much anticipated interest rate announcement on July 31st. There had been much buildup heading into the meeting that the Fed would potentially cut 50bp and communicate an even more troublesome global economic outlook, however Jerome Powell simply delivered the 25bp “insurance” cut that was largely priced into markets, called it a “mid-cycle adjustment” and said it was not the start of a rate cutting cycle. The “Fed rate cut trade” initially didn’t like the sound of that and so bonds and Eurodollar prices traded lower and the USD spiked higher across the board. USDCAD, in particular, broke its downtrend since June with a bullish outside day close above the key 1.3200 resistance level. However, interest rate traders quickly saw through the Powell puppet show of false confidence and violently took bond and Eurodollar prices scorching higher the following day. Attention also started to once again focus on the offshore dollar/yuan exchange rate as well, which had now broken out of its narrow price range for July and made a bee line for the 6.95-6.96 key resistance level. Sure enough (as if the USDCNH chart saw it coming), we then got the bombshell out of the Trump administration in the form of a surprise, new 10% tariff on an additional $300bln of Chinese imports, which would kick in effective Sep 1st. This sent global equities, the Chinese yuan, and commodity currencies lower to start the month of August, but the panic really set in last Monday when China’s PBOC decided not to defend the 7.00 level in its daily USDCNY fix. Pandemonium hit stock prices and interest rates collapsed across the globe as the trade war now took a turn for the worse. A surprise 50bp cut to interest rates from the Reserve Bank of New Zealand on Monday night then further added to the “risk off” mood in markets and before we knew it USDCAD was threatening the next major trend-line resistance level at the low 1.33 level. A sense of calm returned to global markets last Tuesday and Wednesday however after the PBOC announced a large bond sale in Hong Kong (a monetary policy tool that has typically created demand for yuan) and after the PBOC set the daily USDCNY fixes lower than what traders were expecting. Lower than expected PBOC fixes seemed to be the theme for the rest of the week last week (perhaps in response to the US Treasury formally labelling China a currency manipulator), and so global markets have calmed down a bit (equities, commodity currencies and bond yields off their lows). September crude oil prices, initially hit after the Fed meeting and last week’s global risk off wave in equities, are also trading well of their August lows and we think Friday’s rhetoric from Saudi Arabia about how it will consider all options to halt a drop in oil prices is helping with that. All this “calming down” is seeing USDCAD retreat back to the low 1.3200 level it broke above after the Fed meeting, but the technical outlook for the market now appears non-directional in our opinion. This week’s calendar features the US CPI report for July (tomorrow); US Retail Sales for July, US Industrial Production for July, the Philly Fed survey for August, and the Canadian ADP employment report for July (all on Thursday); and finally the July Housing Starts and Building Permit data out of the US (on Friday). The leveraged funds at CME (which piled into new short USDCAD positions over the last month) are now licking their wounds as the market moves against them, but they continue to hold a net short position to the tune of 24k contracts (as of Aug 6th). We view near term support in USDCAD at 1.3195-1.3210, and near term resistance in the 1.3240s, then 1.3275.

USDCAD DAILY

USDCAD HOURLY

SEP CRUDE OIL DAILY

EURUSD

Euro/dollar has been all over the map over the last two weeks. Disappointment from the rate cutting crowd following the Fed meeting saw chart support in the low 1.11s finally give way and we saw the market extend to new lows for the year. A trend-line extension level off the market’s May 2019 lows then came to the rescue in the 1.1030s, along with the plunge in US yields that followed on August 1st. The surprise announcement of new tariffs on China effective Sep 1st then unleashed a wave of “risk-off” across markets that saw December gold prices and EURUSD surge higher at the beginning of last week, and since then the market has been dealing with a mess of chart resistance in the 1.1210-1.1250 area. Election uncertainty officially re-entered Italian politics late last week with League leader and deputy PM Salvini’s announcement that a new election is the only path forward. Traders are now eyeing a meeting that is set to occur this week between all coalition partners and the Italian President to set the date for a confidence vote that is likely to be the trigger for new elections. This week’s calendar will also feature the German ZEW survey for August (tomorrow), German Q2 and Eurozone Industrial Production for June (Wednesday) and a number of European market closures on Thursday (Assumption Day holiday in France and Italy). The leveraged funds at CME remain net short the market to the tune of 44k contracts (as of Aug 6th) and we think gold's ascent to new highs above the $1500 mark is giving these traders something to think about. The euro had a rough open to the week this morning after the German 10yr bund yield opened closer and closer to the -0.60% level and EURUSD lost chart support in the 1.1180s, but the market has fully recovered heading into NY trade, which is leading us to believe the market now has some momentum to challenge the chart resistance it was dealing with from last week.

EURUSD DAILY

EURUSD HOURLY

DEC GOLD DAILY

GBPUSD

Sterling is bouncing higher this morning, but from very depressed levels after an abysmal Q2 GDP figure for the UK saw the market collapse further on Friday. Today’s bounce feels technical and flow driven as there is not much Brexit news to digest. Horizontal chart support in the 1.2030s (from January 2017) has been regained. The EURGBP cross is struggling at trend-line extension resistance in the 0.9320s. What is more, EURUSD is now gone green for the session, which appears to be leading some broad USD selling at this hour. This week’s UK economic calendar features the July employment report (tomorrow), July CPI (Wednesday), and July Retail Sales (Thursday), but “no-deal” Brexit risk will likely continue to be the focus for GBPUSD after Dominic Raab confirmed on July 29th that the UK is “turbo-charging” preparations for the country to leave the EU without an agreement. Technically speaking, the market looks in horrible shape. The July 26th breakdown below the July 17th lows in the 1.2370s was significant in our opinion and since then multiple attempts to regain downward sloping trend-line extensions in the high 1.21s have failed. Parity calls (GBPUSD = 1.00) are now making the rounds should no-deal Brexit become a reality on Oct 31st. Talk is also swirling that the Labour party will threaten a vote of non-confidence against PM Boris Johnson when politicians return from the summer recess on Sep 3rd. We think GBPUSD remains a sell on rallies. The leveraged funds at CME extended their net short position to new highs (now 100k+ contracts) during the week ending August 6th.

GBPUSD DAILY

GBPUSD HOURLY

EURGBP DAILY

AUDUSD

The Fed meeting really took the floor out from underneath the Aussie, but the very poor price performance from the week prior was a harbinger to that in our opinion. The July 29th move below chart support at the 0.6900 level started the cascade lower and the broad USD buying that followed Powell's less dovish than expected rate cut simply added fuel to the fire. The escalation in the US/China trade war early last week and resulting collapse in the Chinese yuan gave AUDUSD another sucker punch, as did the surprise 50bp rate cut from the RBNZ last Tuesday night. The market has since bounced as the PBOC attempts to calm the markets down, but downward sloping trend-line resistance in the high 0.67s / low 0.68s continues to find sellers. This week’s calendar features the July NAB survey (tonight at 9:30pmET), the Westpac August Consumer Confidence data and Q2 Wage Price Index (tomorrow), a speech from the RBA’s Debelle (early Wednesday) and finally the July employment report (Wednesday night). We would not be surprised to see AUDUSD re-test trend-line support at the 0.6700 level at some point over the next week or so. The leveraged funds at CME extended their net short position for a second week in a row during the week ending August 6th, and the position now stands at 55k contracts.

AUDUSD DAILY

AUDUSD HOURLY

USDCNH DAILY

USDJPY

Dollar/yen is starring further into the Jan 3rd flash crash abyss this morning as last week’s support in the 105.50s has now given way. It is quite clear at this point that the bond markets are not believing the Fed and this is leading to a resumption of the collapse in interest rates worldwide. German bund yields now yield close to -0.60%, the US 10yr yield has fallen back below 1.70% after last week’s panic bounce off the 1.60% level, and the Eurodollar futures contract for June 2021 (the peak month of the currently inverted yield curve) says we could see Federal funds closer and closer to 1% as “things” get worse. Jerome Powell hinted that it could be something else during the Fed meeting, when he said “manufacturing is weak all over the world, but I wouldn’t lay that all at the doorstep of trade”. We still think markets, and more particularly banks, are concerned about some sort of liquidity event on the horizon and that’s the reason they’re perfectly comfortable hording high quality government paper, even if it costs them to do so. The leveraged funds at CME flipped decisively to a net short position in USDJPY during the week ending Aug 6, by liquidating long positions and adding to short positions. We think the 105.50-70 level will be a key pivot for the market this week. A rally back above could make this new fund position nervous while staying below the level should keep traders focused on what lies below 105.00.

USDJPY DAILY

USDJPY HOURLY

US 10YR BOND YIELD DAILY

Charts: TWS Workspace

About the Author

Erik Bregar - Director, Head of FX Strategy

Erik works with corporations and institutions to help them better navigate the currency markets. His desk provides fast, transparent, and low cost trade execution; up to the minute fundamental and technical market analysis; custom strategy development; and post-trade services -- all in an effort to add value to your firm’s bottom line. Erik has been trading currencies professionally and independently for more than 12 years. Prior to leading the trading desk at EBC, Erik was in charge of managing the foreign exchange risk for one of Canada’s largest independent broker-dealers.

Interested in creating a custom foreign exchange trading plan? Contact us or call CXI's trading desk directly at 1-833-572-8933.

Currency Exchange International (CXI) is a leading provider of foreign currency exchange services in North America for financial institutions, corporations, and travelers. Products and services for international travelers include access to buy and sell more than 80 foreign currencies, gold bullion coins and bars. For financial institutions, our services include the exchange of foreign currencies, international wire transfers, purchase and sale of foreign bank drafts, international traveler’s cheques, and foreign cheque clearing through the use of CXI’s innovative CEIFX web-based FX software www.ceifx.com