Recession fears grow as the 10s2s yield curves go inverted in the UK and the US

Take control of your international payments with CXI FX Now.

• Zero transfer fees & great rates

• Fast international payments

• Safety and security

• Unparalleled customer service

• Consultative approach

Learn more about CXI's international payment services for businesses or call our trading desk directly at 1-833-572-8933.

Get real-time market coverage on twitter at @EBCTradeDesk or sign up here.

SUMMARY

ANALYSIS

USDCAD

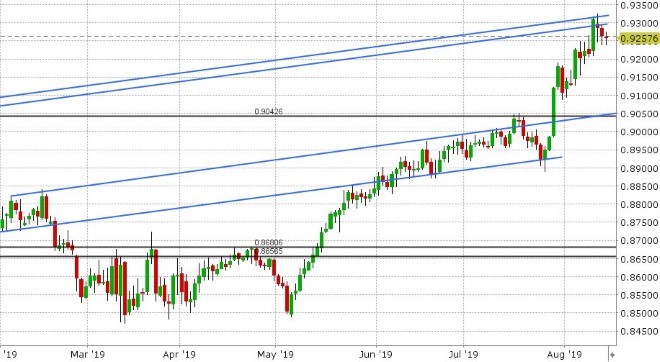

Dollar/CAD has gone on a wild ride over the last 24hrs, but we’d still argue we’re trading with a range-bound, non-directional, tone since the start of the week. Yesterday’s hotter than expected headline and core inflation reads from the July US CPI report saw broad USD buying initially, but this move started to reverse after traders focused on the report’s weakening trend for wage growth. A couple of positive US/China trade headlines then lit a fire under risk assets which sent stocks, oil prices, the Chinese yuan and commodity currencies soaring higher while bonds, eurodollar futures, the USD and the JPY all collapsed lower. The first headline said that Chinese Vice Premier spoke with USTR Lighthizer and Treasury Secretary Mnuchin (at the US’s request) and that negotiations were set to resume within the next two weeks. The second headline said that some Chinese products will be removed from the “10% additional tariff” list based on health, safety, national security and other factors. It didn’t appear as if the Trump administration got anything from China in return for softening its stance so quickly, but traders drank the Kool-Aid and stuck to “risk-on” for most of the session yesterday, which saw USDCAD fall all the way back down to trend-line support in the 1.3180s. Buyers swooped in however and pushed the market back the 1.3200 mark into the NY close, which made the technicals look a bit more positive. The overnight session has been a doozy to say the least. We got bad economic news out of China (July Industrial Production +4.8% vs +5.8% exp, July Retail Sales +7.6% vs +8.6% exp), more bad news out of Germany (a -0.1% contraction to Q2 GDP), even worse Industrial Production data for the Eurozone (-2.6% YoY vs -1.2% exp for June + a downward revision for May’s data from -0.5% to -0.8%) and an inversion in the 10s2s yield curve in the UK. This saw yesterday’s “risk-on” move start to unravel during the European morning, which brought back broad demand for USD. Then we got the headline that everybody’s been waiting for…the widely followed US 10s2s treasury curve has finally inverted, and that last time this happened we were in the 2008 global financial crisis! None of this comes as a surprise to us as yield curves all over the place have been inverting for some time now (Eurodollars, swaps, US 10s vs 3month) and so in our opinion this was simply a matter of time. Needless to say, US recession fears are running rampant this morning, which is leading stocks and oil prices to decline further. USDCAD is now re-testing yesterday’s session highs around trend-line resistance in the 1.3280s and gold prices have recouped 2/3 of yesterday’s losses. Today’s North American data docket doesn’t feature any important economic releases but the financial media should have plenty of recession debate to chew on. The EIA reports its weekly oil inventory report at 10:30amET as usual, and traders here are looking for a build of almost 5mln barrels following last night’s surprisingly bearish API report (+3.7M barrels vs -2.77M expected), which goes against the seasonal trend of draws. We think USDCAD could inch higher to the 1.3320s given this morning’s broad “risk-off” momentum, and we think the odds of a larger trend reversal increase significantly with a move above last week’s highs in the 1.3340s.

USDCAD DAILY

USDCAD HOURLY

SEP CRUDE OIL DAILY

EURUSD

Euro/dollar gave up on its quest to get above the 1.1210s yet again yesterday. While this market hasn’t been a huge mover off US/China trade related headlines, it succumbed to the dramatic reversal lower in gold prices in our opinion, as EURUSD has been following that market again since the US announced the threat of new tariffs on China last week. Yesterday’s selling took EURUSD below trend-line support in the 1.1190s, and while gold prices are reversing higher this morning in light of today’s global “risk-off” mood, the market has failed on two occasions to regain this level. We think this technical failure, along with today’s broad demand for USD could keep EURUSD on the defensive here.

EURUSD DAILY

EURUSD HOURLY

DEC GOLD DAILY

GBPUSD

Sterling appeared to catch a bid off the better than expected UK CPI data out for July this morning (+2.1% YoY vs +1.9% expected), but GBPUSD appears to also be dealing with a technical failure on the charts. Traders attempted a move above familiar, downward sloping, trend-line resistance (now in the 1.2090s) but they’ve given up and are now selling as both the UK and US 10s2s yield curve inversions spook global markets. UK PM Boris Johnson said this morning the EU is “not compromising at all” on the Brexit deal and that the longer this situation goes on, the more likely the chance the UK leaves the EU without a deal.

GBPUSD DAILY

GBPUSD HOURLY

EURGBP DAILY

AUDUSD

The Aussie is feeling the full brunt of today’s global “risk off” wave. The Australian data released last night was ok (+3.6% for Aug Consumer Confidence vs -4.1% previously…and +0.6% QoQ growth for the Wage Price Index in Q2 vs +0.5% expected) but the weak Chinese and European data points released overnight are casting a gloomy shadow over broad risk sentiment in general. This morning’s treasury yield curve inversions in the UK and the US are certainly not helping, and so we see AUDUSD searching for buyers once again. We still think traders should be prepared for a re-test of the low 0.67s. USDCNH is bouncing higher with this morning’s broad demand for USD, and we would note yesterday’s ability for the market to hold the psychological 7.00 as technically positive. The RBA’s Debelle will be making a speech later today at 7pmET. Australia reports its July employment report at 9:30pmET, with traders are expecting +14k new jobs and 5.2% on the unemployment rate.

AUDUSD DAILY

AUDUSD HOURLY

USDCNH DAILY

USDJPY

Dollar/yen is also dialing back yesterday’s US/China trade headline euphoria this morning as global bond markets continue to signal things are going to get worse, not better. We already mentioned today’s US 10s2s yield curve inversion. US 10yr yields, on their own, are now risking a collapse to new record lows below 1.60%. The German bund traded to a new record low yield about an hour ago (-0.65%). Ditto for French 10yr yields (-0.35%). Spain’s 10yr looks like it’s going to be the next one to go below zero. What is more, we now have the US 30yr bond yield trading below the effective fed funds rate, which is unprecedented! Something is not right in the global economy, it’s getting worse, and we’re now getting more and more convinced that world money markets are bracing for a wider USD liquidity problem. Central bankers wouldn’t dare say this as it discredits everything they’ve attempted with quantitative easing and excess reserves. Blaming everything on the ongoing US/China trade war is far simpler to convey and for the public to understand, and hides what we think is really going on and what is far more difficult to explain.

USDJPY DAILY

USDJPY HOURLY

US 10YR BOND YIELD DAILY

Charts: TWS Workspace

About the Author

Erik Bregar - Director, Head of FX Strategy

Erik works with corporations and institutions to help them better navigate the currency markets. His desk provides fast, transparent, and low cost trade execution; up to the minute fundamental and technical market analysis; custom strategy development; and post-trade services -- all in an effort to add value to your firm’s bottom line. Erik has been trading currencies professionally and independently for more than 12 years. Prior to leading the trading desk at EBC, Erik was in charge of managing the foreign exchange risk for one of Canada’s largest independent broker-dealers.

Interested in creating a custom foreign exchange trading plan? Contact us or call CXI's trading desk directly at 1-833-572-8933.

Currency Exchange International (CXI) is a leading provider of foreign currency exchange services in North America for financial institutions, corporations, and travelers. Products and services for international travelers include access to buy and sell more than 80 foreign currencies, gold bullion coins and bars. For financial institutions, our services include the exchange of foreign currencies, international wire transfers, purchase and sale of foreign bank drafts, international traveler’s cheques, and foreign cheque clearing through the use of CXI’s innovative CEIFX web-based FX software www.ceifx.com