Powell disappoints, but the doves still believe

Take control of your international payments with CXI FX Now.

• Low transfer fees & great rates

• Fast international payments

• Safety and security

• Unparalleled customer service

• Consultative approach

Get real-time market coverage on twitter at @EBCTradeDesk or sign up to currency insider here.

SUMMARY

- Powell says Fed’s new 2% inflation target will be an “average”.

- No formula to define “average”. No details on how to get there.

- USD and US yields reverse higher, but Fed’s Kaplan saves the day.

- Kaplan implies Fed not done yet, many FX analysts agree post Jackson Hole.

- USD extends losses overnight, aided by CNY fix & month-end USD sales.

- USDJPY plunge also exacerbates after Abe announces resignation.

ANALYSIS

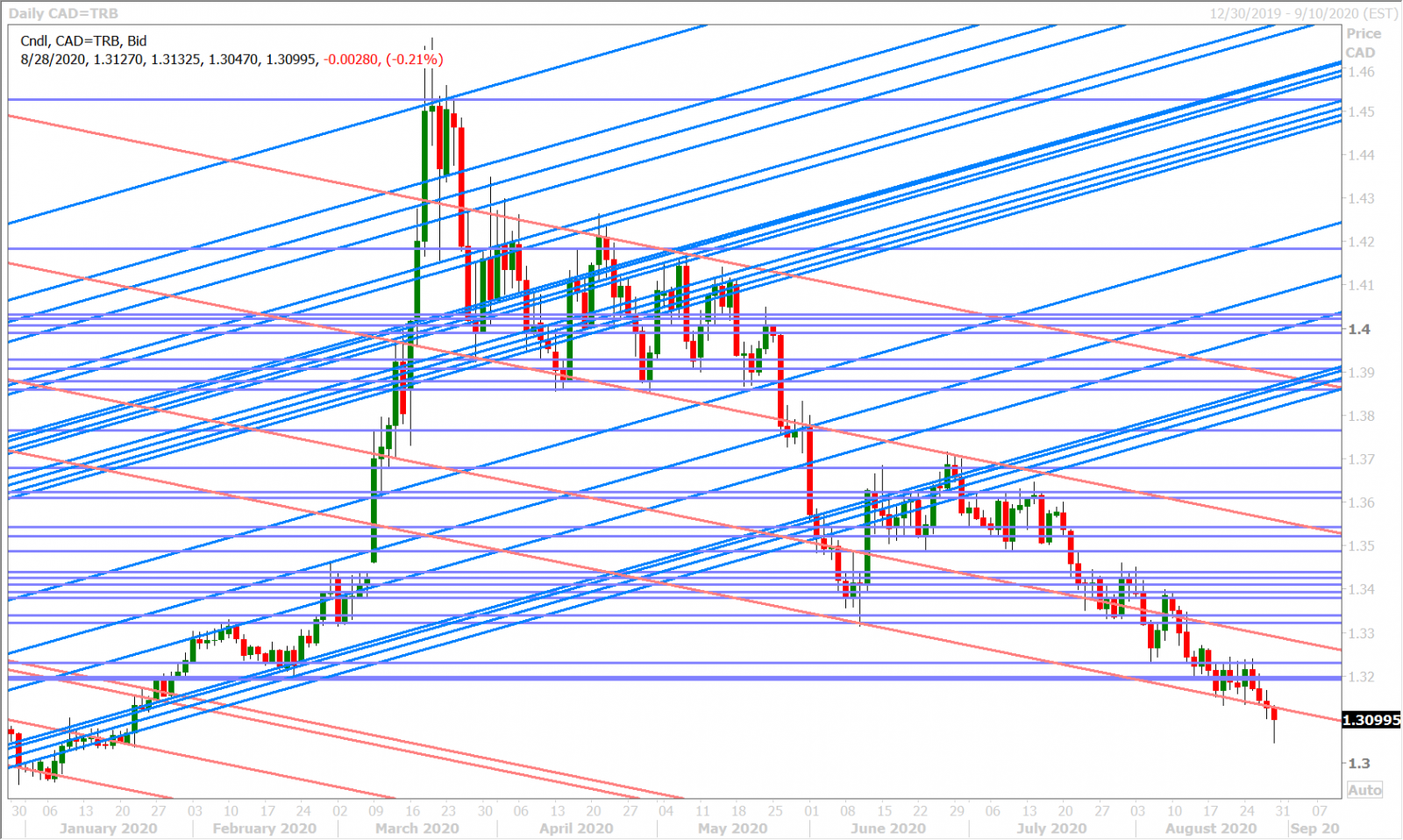

USDCAD

We took the unpopular view yesterday morning that Jerome Powell’s speech at Jackson Hole disappointed markets with its unwillingness to define the Fed’s new “average” 2% inflation target and its lack of detail with regard to how the Fed would ultimately achieve it, after a decade of failed policy towards raising consumer prices. We felt Powell’s remarks didn’t exactly exude confidence to market participants the Fed knew what to do next, from an “actual” policy-tool perspective, and it was this purposeful ambiguity that ultimately prompted entrenched USD shorts to cover their positions after some initial excitement. A sharp reversal higher for US yields supported the USD bounce into mid-day, along with a VIX spike-driven fall in the S&Ps, but this “Fed disappointment” momentum came to an abrupt halt when the Fed’s Kaplan said that the new policy framework is “not a commitment on what the Fed will do”. Risk sentiment broadly recovered after this statement (perhaps on the thought the Fed actually has a new policy tool up its sleeve for the September FOMC meeting?), which in turn left the broader USD to struggle with less than convincing bullish reversal signals into the NY close.

The dollar selling continued in Asia last night after the PBOC fixed USDCNY at another new 7-month low and it snowballed precipitously on USDJPY sales after Japanese PM Shinzo Abe suddenly announced his resignation due to health problems. Talk of month-end USD selling has made the rounds as well and we’d note resounding USD bearishness in Jackson Hole post-mortems from FX analysts this morning, based on the belief that the Fed’s new policy framework will now set the stage for even more accommodative policy action from the FOMC next month...although we think some of this is an over-interpretation of today’s USD weakness (which is arguably due to other reasons as well). We share the bond market’s skepticism about the “actual” path forward until we hear something more definitive from the Fed, but wouldn’t stand in the way of the dollar’s strong downtrend until we see clear signs of seller failure on a NY closing basis.

This morning’s stronger than expected GDP figures out of Canada were a non-event for the USDCAD market because it’s old news (+6.5% MoM for June vs +5.6% and -38.7% YoY for Q2 vs -39.6%). The broader USD recovered a little bit on the back of some mild risk-off flows following a stronger read for July US Core PCE (+1.3% YoY vs +1.2% expected and +0.9% previously), but these flows have now evaporated into the London fix.

USDCAD DAILY

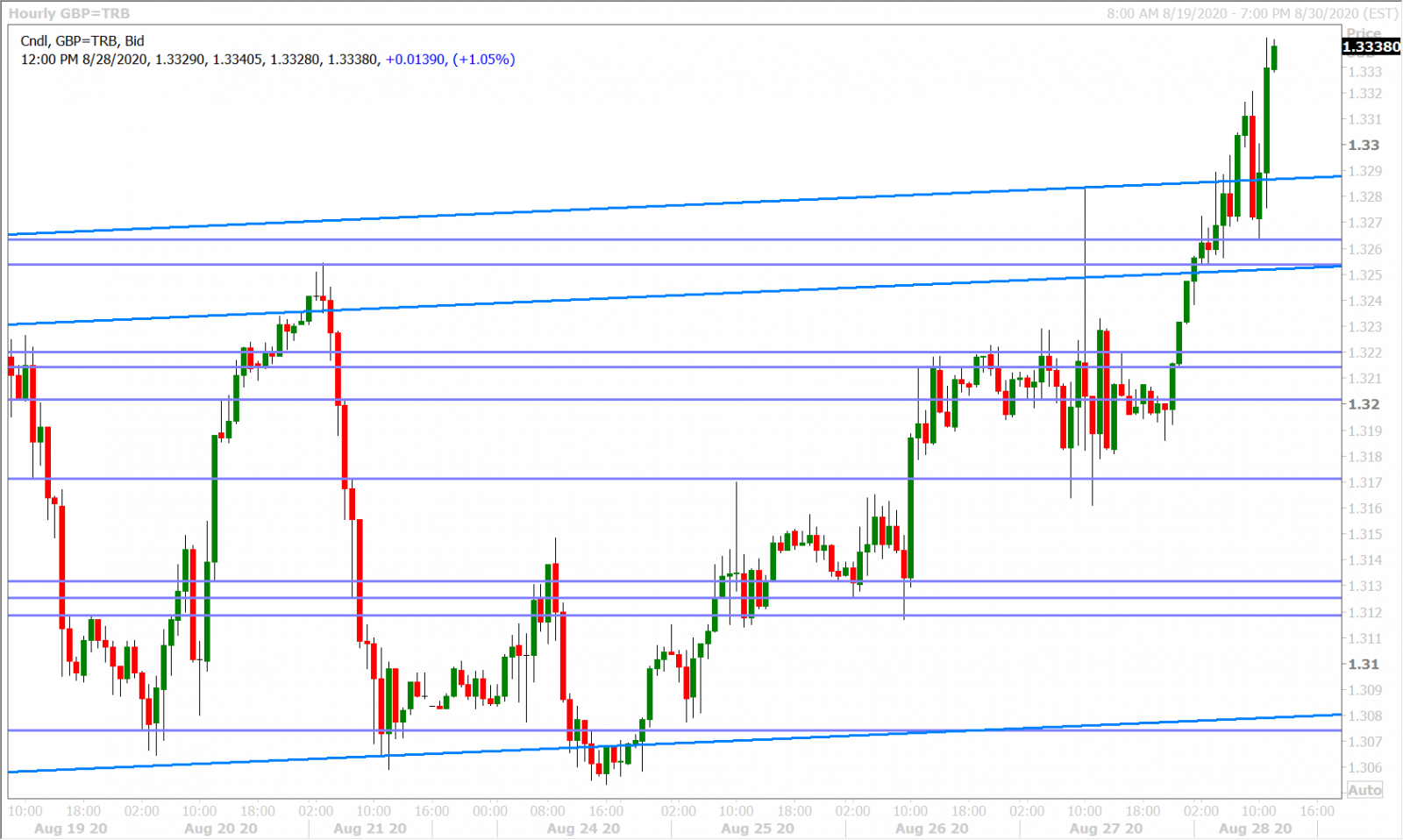

USDCAD HOURLY

OCT CRUDE OIL DAILY

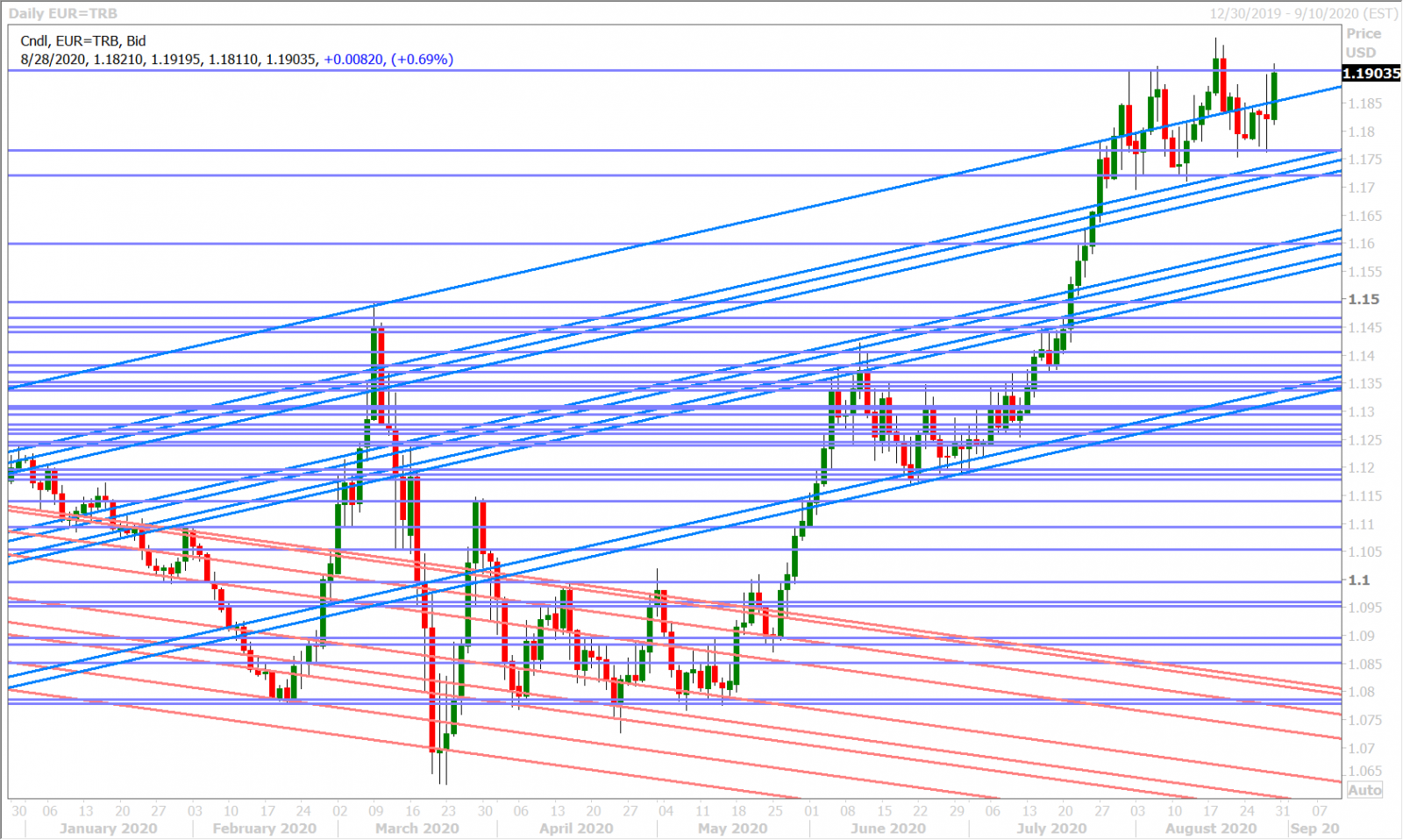

EURUSD

Euro/dollar excitedly punched above the 1.1840s resistance level yesterday as Jerome Powell announced average-inflation-targeting and, while it swiftly reversed lower on “actual” policy-action disappointment into the NY options cut, the buyers staunchly defended familiar chart support in the 1.1760s. We felt that the ECB’s Philip Lane helped with this when he said it would be costly to allow inflation to take more time to reach its target, but then didn’t expand upon his early morning comment about being ready to do more as needed. A short-lived spike in the VIX saw EURUSD briefly retrace, but we think Kaplan’s comments were enough to quell the Powell disappointment and give the market a more neutral chart structure going into the NY close.

Chinese yuan and Japanese yen strength very much led EURUSD higher through the 1.1840s in overnight trade and so we don’t want to read too much into the street’s new found consensus view that the Fed will pull another rabbit (or dove) out of its hat in September. Month-end USD sales are also widely being reported and we’d give credence to this dynamic as well. The market faded 1.1910s chart resistance following some stronger US Core PCE data for July, but new highs for AUDUSD and GBPUSD now seems to be forcing a re-test of this level.

EURUSD DAILY

EURUSD HOURLY

SPOT GOLD DAILY

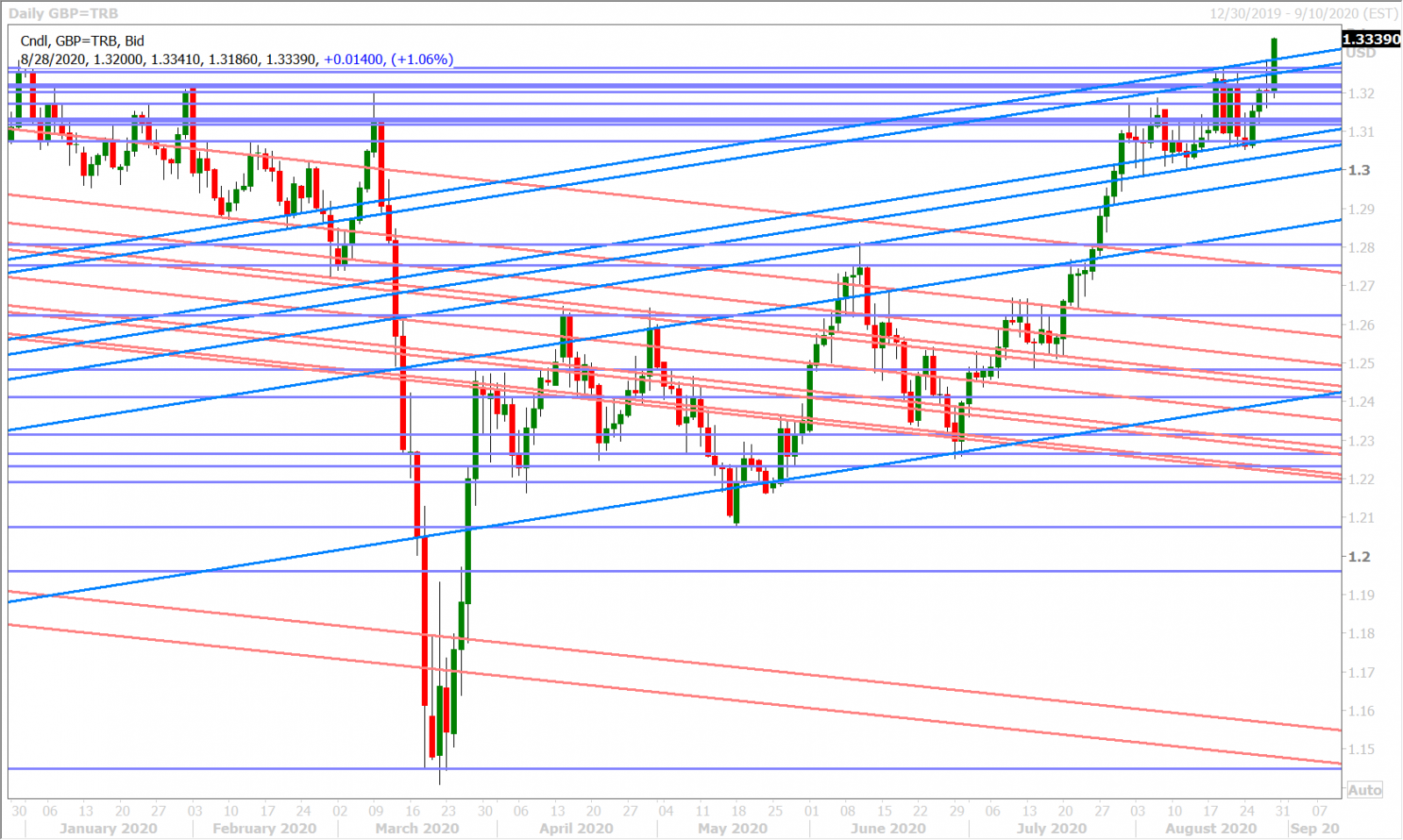

GBPUSD

Bank of England Governor Andrew Bailey said “we are not out of firepower by any means” when he spoke shortly after 9amET on day two of the Jackson Hole symposium, but he didn’t hint at any need for it right now and so we think this largely explains sterling’s out-performance vis a vis the euro since the NY open. Sterling/dollar pulled back below former chart resistance turned support in the 1.3280s after the stronger US inflation numbers this morning, but it has since recouped those losses on a strong bounce off 1.3260s support and now trades at new 8-month highs.

GBPUSD DAILY

GBPUSD HOURLY

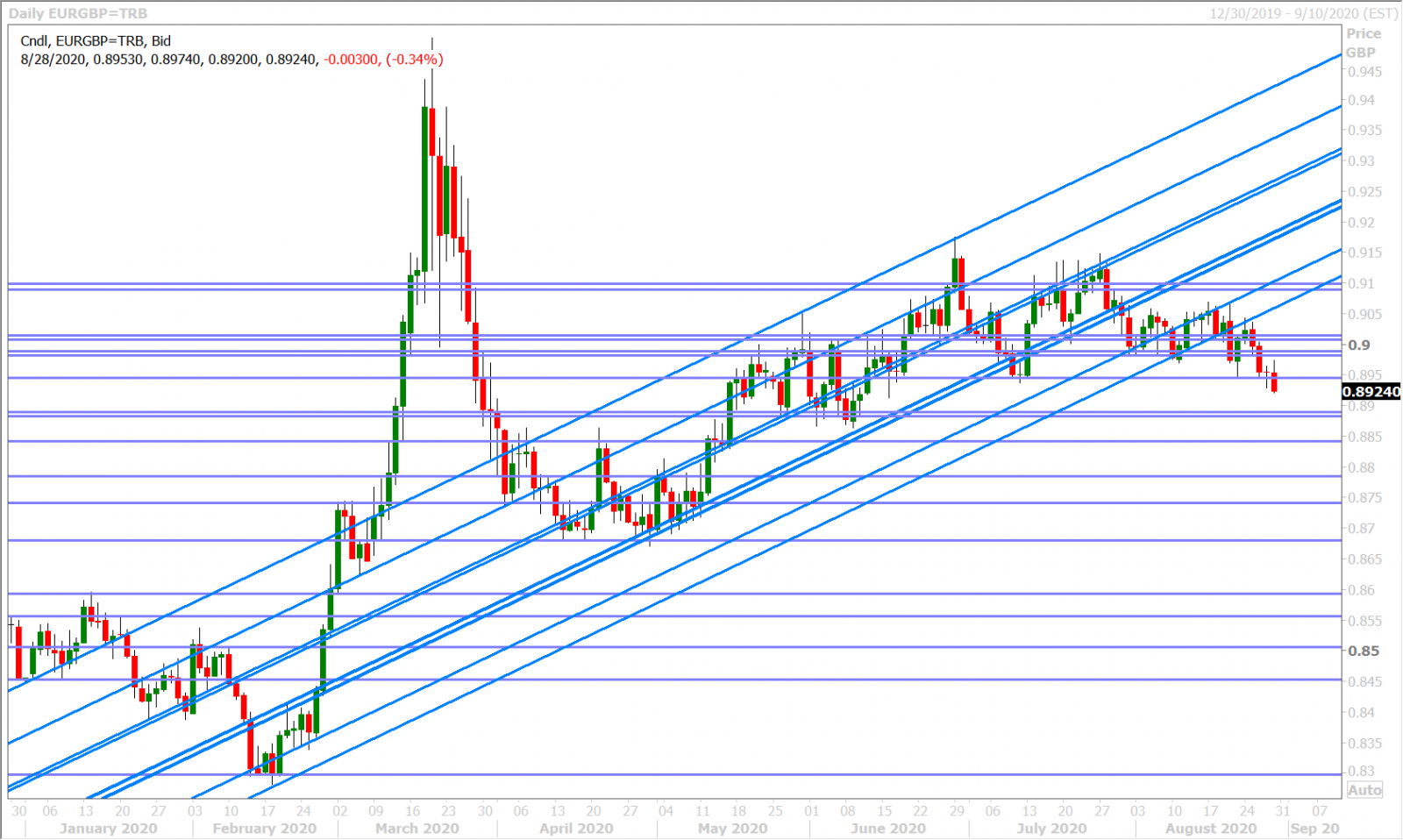

EURGBP DAILY

AUDUSD

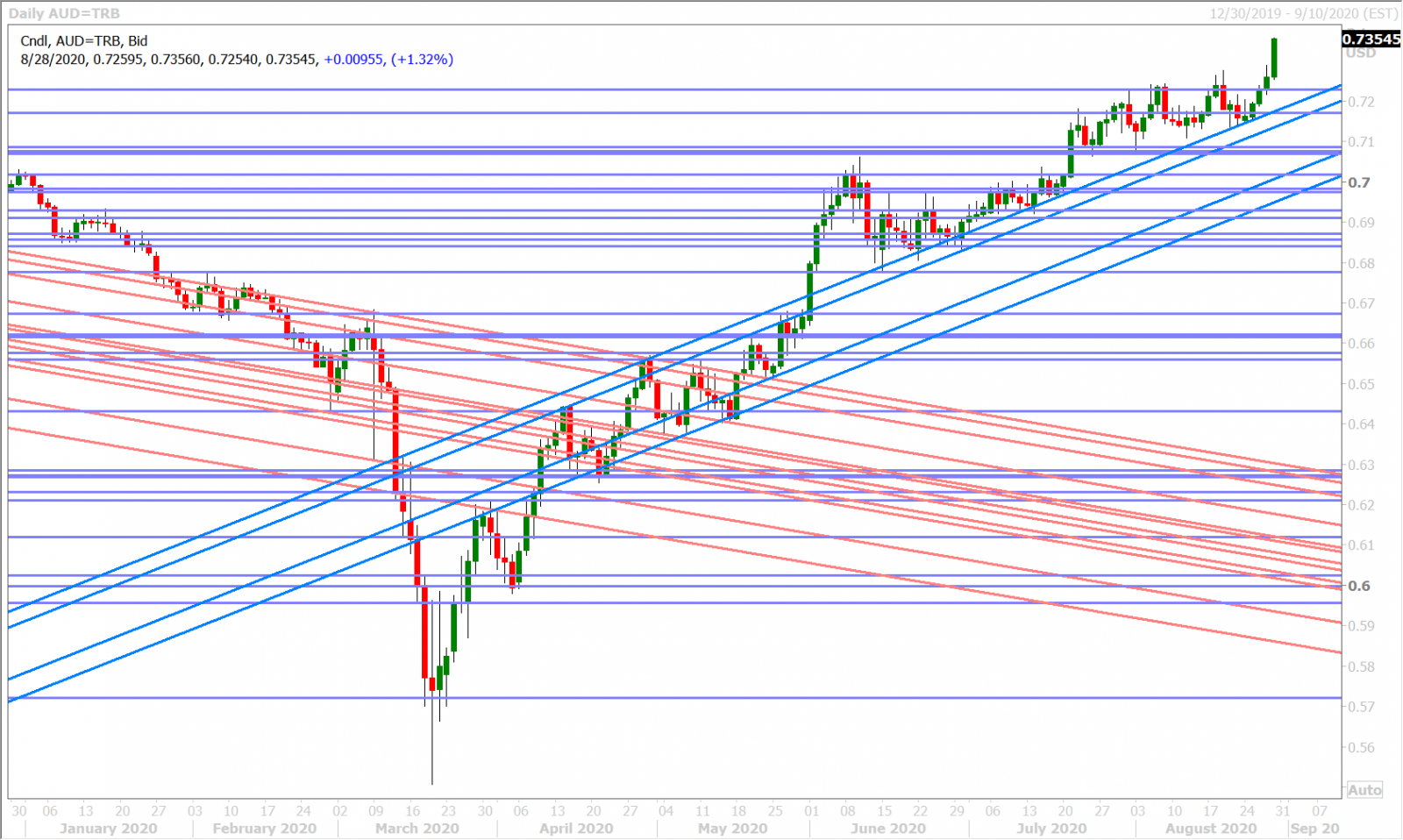

The Australian dollar is charging to new 2-year highs this morning as CNH and JPY strength, month-end portfolio re-balancing flows, and a reassertion of dovish Fed calls from the street (post-Jackson Hole) propels the USD broadly lower. We think today’s upward momentum was very much aided by yesterday’s strong recovery for AUDUSD back above the 0.7230 level into the NY close.

AUDUSD DAILY

AUDUSD HOURLY

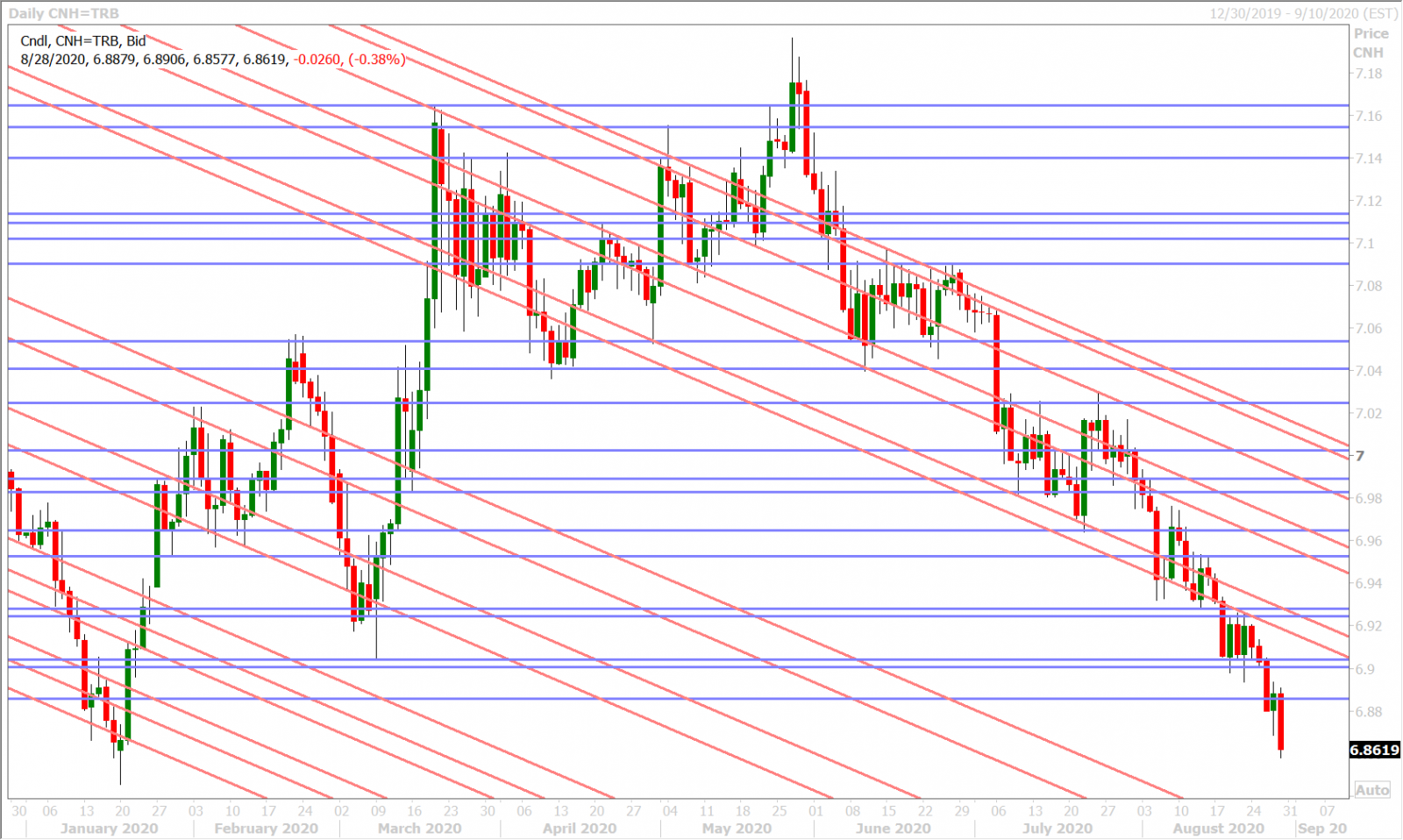

USDCNH DAILY

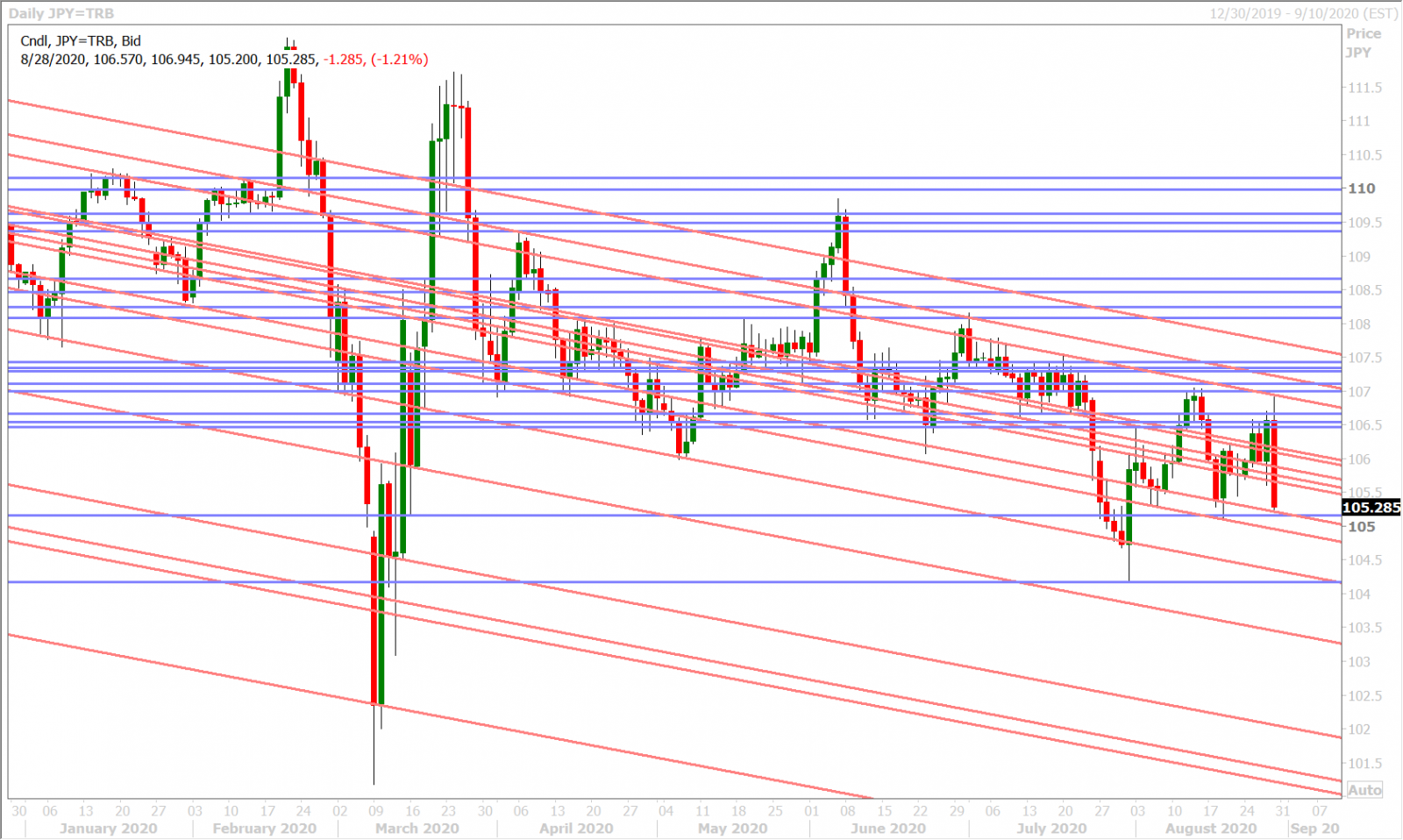

USDJPY

Japanese markets freaked out overnight when Shinzo Abe announced his resignation. While the decision was made due to the Japanese prime minister’s continued struggle with a chronic inflammatory bowel disease, the news seemed to spark fears that the reflationary age of “Abenomics” would now come to an end, from both a fiscal and monetary policy perspective. The initial plunge in USDJPY felt like a bit of an over-reaction, but it’s been worsened now by post-Jackson Hole dovishness and reports of month-end USD selling. This morning’s stronger US Core PCE data for July seemed to help dollar/yen bounce off chart support in the 105.20s, but the market’s swift plunge off the 106.90s resistance level has created a very ominous bearish daily reversal pattern.

USDJPY DAILY

USDJPY HOURLY

US 10YR BOND YIELD DAILY

Charts: Reuters Eikon

About the Author

Erik Bregar - Director, Head of FX Strategy

Erik works with corporations and institutions to help them better navigate the currency markets. His desk provides fast, transparent, and low cost trade execution; up to the minute fundamental and technical market analysis; custom strategy development; and post-trade services -- all in an effort to add value to your firm’s bottom line. Erik has been trading currencies professionally and independently for more than 12 years. Prior to leading the trading desk at EBC, Erik was in charge of managing the foreign exchange risk for one of Canada’s largest independent broker-dealers.

Interested in creating a custom foreign exchange trading plan? Contact us or call CXI's trading desk directly at 1-833-572-8933.

Currency Exchange International (CXI) is a leading provider of foreign currency exchange services in North America for financial institutions, corporations, and travelers. Products and services for international travelers include access to buy and sell more than 80 foreign currencies, gold bullion coins and bars. For financial institutions, our services include the exchange of foreign currencies, international wire transfers, purchase and sale of foreign bank drafts, international traveler’s cheques, and foreign cheque clearing through the use of CXI’s innovative CEIFX web-based FX software www.ceifx.com